Indian professionals who are moving back from the UAE often lack clarity about how they can manage their overseas holdings like global stocks, ETFs, and UAE investment accounts after returning to India.

This article explains how you can manage your global holdings after moving back to India, and the Indian tax and reporting requirements you will be subject to.

We also cover your tax residency status, how it changes, and how you can use RNOR rules to extend the tax-free benefits you enjoyed in the UAE.

Table of contents

- What happens to my stocks when I move back

- Best way to stay invested globally after moving back

- Tax and reporting implications of moving back

- RNOR status and how it affects you

What happens to my stocks when I move back to India?

Most brokerage firms used by expats in Dubai and Abu Dhabi are designed to serve UAE residents. When you move back to India, your tax residency changes, and many platforms are not equipped to handle accounts that comply with Indian tax and foreign exchange laws.

Here is how different platforms typically handle the move:

- Local UAE Platforms (Sarwa, Baraka, Wio Invest): These platforms are built heavily around UAE residency. If you update your KYC address to India or they detect a permanent change in your tax status, they may restrict your account, pause your ability to add new funds, or in some cases, force you to liquidate your positions entirely.

- Global Brokers (Interactive Brokers, Saxo Bank, Swissquote): These international brokers are more flexible and usually allow you to convert your profile to an Indian resident account. However, you will likely face operational hurdles. You are left to manage complex Indian tax reporting manually (like Schedule FA), you face restrictions on certain funds, and funding the account from India going forward can incur high wire transfer fees and poor FX rates.

What's the best way to stay invested globally after moving back to India?

The best way to stay invested globally after moving back to India is transferring your investments into a platform that is specifically made for global investing from India.

These platforms will allow you to maintain your positions and trade as usual, while providing India-specific compliance support like filing Form W-8BEN (for investments in the US) and generating tax documents tailored for Indian reporting requirements.

Tax and reporting implications of moving back to India

When you permanently return to India from the UAE, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

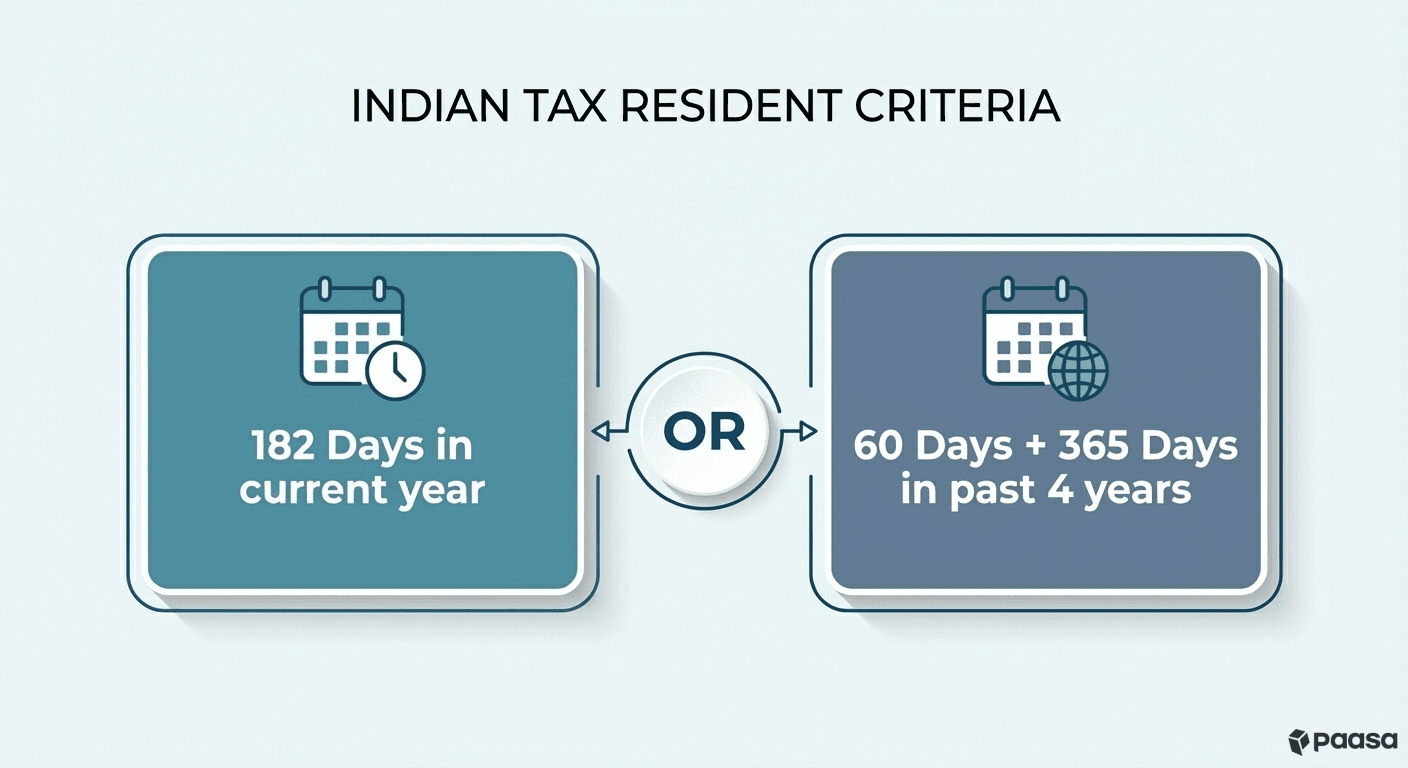

When do you become an Indian Tax Resident?

Under the Income Tax Act, you are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in the four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world.

What is RNOR status and how does it affect me?

As a UAE expat, you are used to a tax-free environment. RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status that effectively extends this tax-free status for your global income for a few years even after you become a tax resident in India.

It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You typically qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

This status grants you a 1 to 3-year window where your global income is treated entirely differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your overseas assets without immediate tax liability.

- Global Stocks & ETFs: If you sell them while you are RNOR, the capital gains are completely tax-free in India. Since the UAE does not levy capital gains tax either, you effectively pay 0% tax. You can use your UAE tax residency and RNOR window to sell your stocks, reset your cost basis, and reinvest without a tax penalty.

- Foreign Bank Interest: The interest earned in your UAE or offshore bank accounts remains tax-free in India.

- Dividends: Dividends earned from global stocks remain tax-free in India during this period.

To utilize these exemptions, you must receive the funds in your foreign bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable immediately.

Common Questions NRIs Have About Moving Back from UAE

Can I send money from India to fund my global investments?

Yes. You can remit up to $250,000 per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks or ETFs.

However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source). This is an advance tax that you can claim back as a refund or adjust against your tax liability when filing your income tax return in India.

To learn more about how you can send money abroad while complying with Indian regulations, read our Complete LRS Guide for Indians.

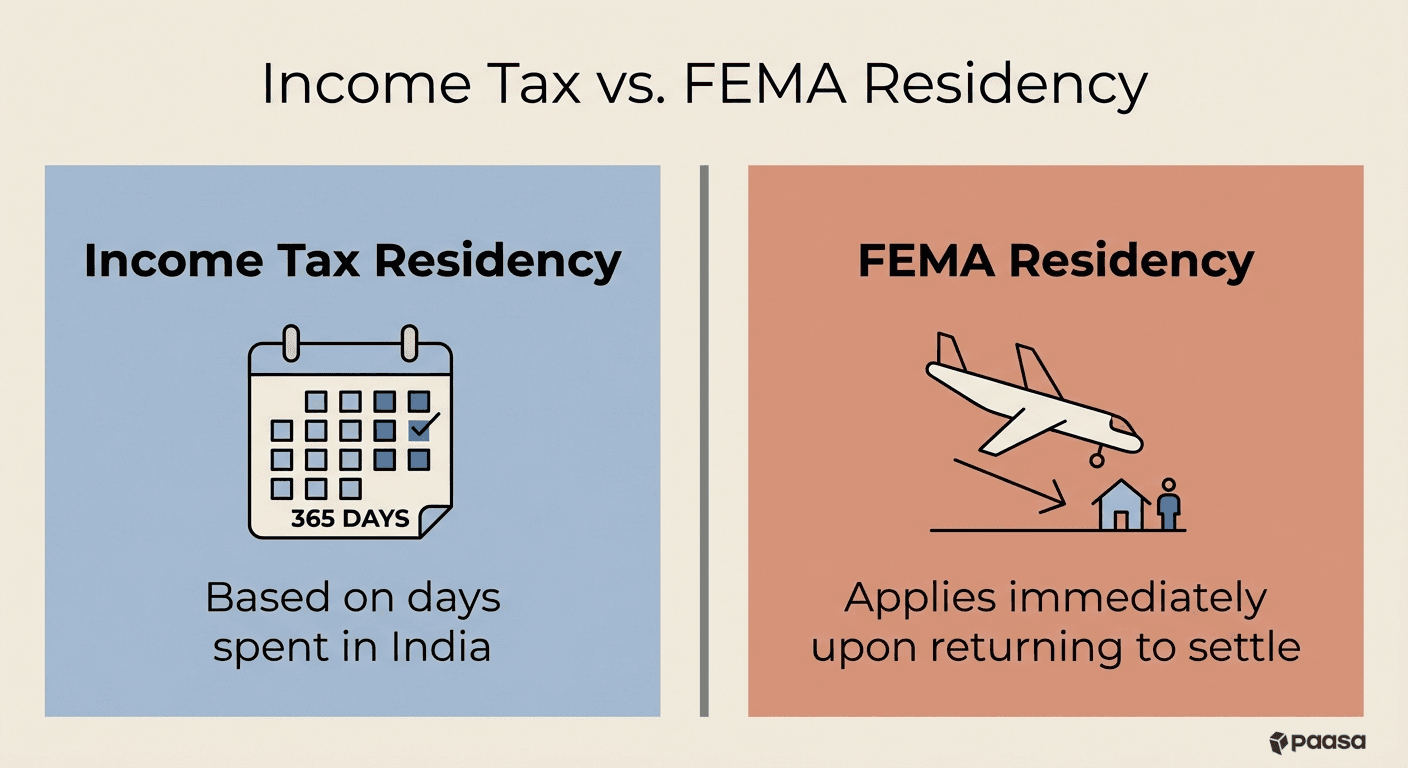

When do I become subject to FEMA upon moving back?

You become a resident under the Foreign Exchange Management Act (FEMA) immediately upon landing in India if your intention is to stay for an uncertain period or for employment and business.

Unlike income tax residency (which counts the number of days you stay), FEMA residency applies the moment you return to settle.

Can I continue operating my UAE bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, overseas stocks, and properties if they were acquired when you were a resident outside India. You are not legally required by the Indian government to close your Dubai or Abu Dhabi bank accounts.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO and NRE accounts to a standard Resident Savings Account. Continuing to hold an NRO or NRE account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore, and we support 9 global currencies.

- Seamless "In-Kind" Transfers: You can move your entire global stock portfolio (from international brokers like Interactive Brokers, Saxo, or Swissquote) directly to Paasa. This allows you to consolidate your assets in one place without selling them and triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures. We eliminate the need for manual calculations for Schedule FA and capital gains.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents holding US-domiciled assets.