When you are remitting funds overseas under the Liberalised Remittance Scheme (LRS), the Tax Collected at Source (TCS) temporarily locks up a significant portion of your capital.

For example, if you have remitted ₹20 lakhs abroad for investments in this financial year, you have paid a TCS of ₹4 lakhs on this transaction, over and above the transaction value (the first ₹10 lakhs is exempt, TCS of 20% is applicable after that).

Waiting until you file your annual income tax return to claim this refund creates an inefficient drag on your cash flow.

However, you do not have to wait for a refund to free up this capital. You can adjust the TCS you have already paid against your advance tax liability.

Here is how you can use your TCS credits to reduce your advance tax and prevent your capital from getting stuck.

Table of contents

- What is advance tax?

- Who is liable to pay advance tax?

- How is advance tax collected?

- Offsetting advance tax with TCS

- TCS rates for foreign remittances

- How to offset advance tax using TCS

- How Paasa helps with tax

What is advance tax?

In India, income tax operates on a "pay as you earn" principle. Instead of paying your entire tax bill as a single lump sum at the end of the financial year, the Income Tax Department requires you to pay it in installments throughout the year as you earn the income.

Who is liable to pay advance tax?

You are legally required to pay advance tax if your estimated total tax liability for the financial year is ₹10,000 or more after deducting any Tax Deducted at Source (TDS).

This applies to all categories of taxpayers (salaried individuals with additional income, freelancers, and businesses) with one specific exception:

- Exempted Category: Resident senior citizens (aged 60 years or older) who do not have any income categorized under "Profits and Gains of Business or Profession" (PGBP) are exempt. They do not have to pay advance tax even if their tax liability from other sources (like pension or interest) exceeds ₹10,000.

How is advance tax collected?

Advance tax is paid online through the Income Tax Department’s e-filing portal using Challan 280 (selecting '100 - Advance Tax' as the type of payment). The collection mechanism depends on your primary source of income.

For salaried employees

Your employer deducts tax directly from your salary (TDS). While TDS serves a similar purpose to advance tax, your employer only calculates this based on your salary.

If you have additional income sources (such as capital gains from stocks or rental income), you have two options:

- Pay it directly: Calculate the tax on the extra income and pay it online via the tax portal.

- Declare it: Disclose your "other income" to your HR department. They will recalculate your tax and increase your monthly TDS deductions to cover the liability, saving you the administrative hassle of paying advance tax separately.

For people engaged in business

If you run a business or work as an independent contractor, you are responsible for calculating and paying the entire tax bill yourself.

The payment schedule depends on your taxation scheme:

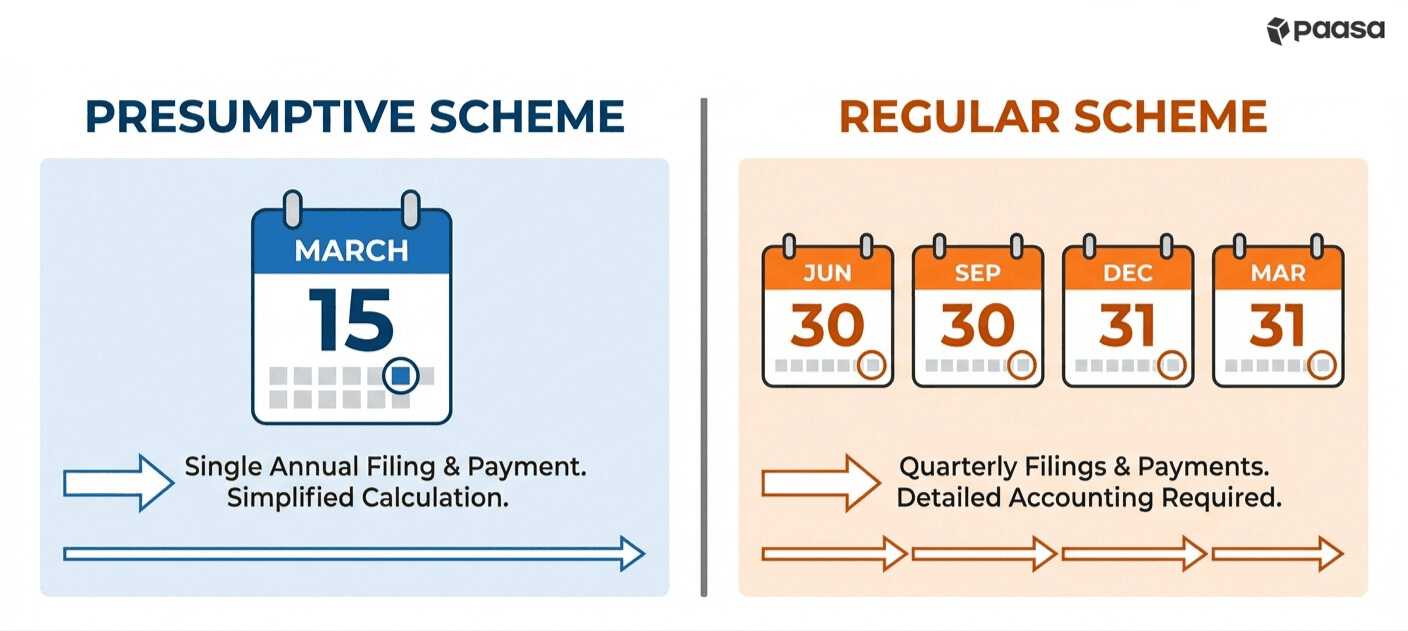

- The Presumptive Scheme (Section 44AD/44ADA): If you opt to declare a fixed percentage of your turnover as presumed profit, you enjoy a simplified schedule. You only need to pay your advance tax in a single installment by March 15th.

- The Regular Scheme: If you declare actual profits by deducting business expenses from your revenue, you must estimate your annual income and pay the advance tax in four quarterly installments (June, September, December, and March).

Can I offset my advance tax liability using the TCS I have already paid?

Yes. You can directly reduce your calculated advance tax liability by the exact amount of TCS you have already paid on foreign remittances.

For global investors, this is the most efficient way to solve the "stuck capital" problem. Instead of letting your TCS sit with the government until you process a refund the following year, you utilize that credit immediately to reduce the tax you owe on your current income (like salary or business profits).

TCS rates for foreign remittances (2026)

| Type of Remittance | Exemption Threshold (Per FY, Per PAN) | TCS Rate (Above Threshold) |

|---|---|---|

| Education (Funded via Loan u/s 80E) | Nil (Fully Exempt) | 0% |

| Education (Self-Funded / Others) | ₹10 Lakhs | 2% |

| Medical Treatment Abroad | ₹10 Lakhs | 2% |

| Overseas Tour Packages | No Exemption | 2% |

| Other Purposes (Investments Gifts etc.) | ₹10 Lakhs | 20% |

To learn more about LRS limits and TCS slabs, read our Complete LRS Guide for Indians (2026).

How to offset advance tax using TCS

The exact mechanics of claiming this offset depend on whether you are employed or running a business.

For salaried employees

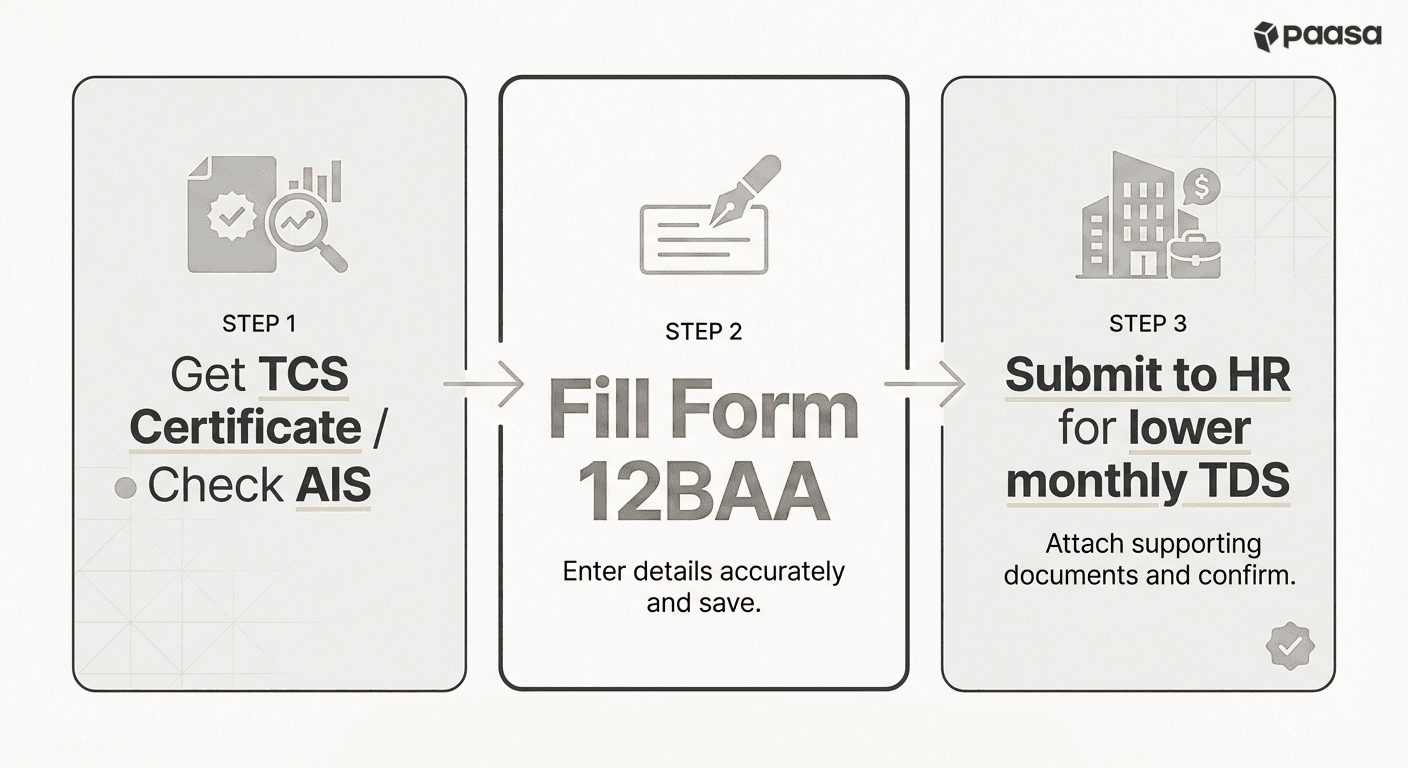

Earlier, salaried individuals had to wait to claim TCS as a refund. Now, you can adjust it directly against your monthly salary TDS, instantly increasing your monthly take-home pay.

- Obtain your TCS Certificate (Form 27D) from your bank/broker, or verify the TCS amount reflected in your Annual Information Statement (AIS) on the tax portal.

- Fill out Form 12BAA. This is a specific declaration form used to report "other taxes paid," including TCS on foreign remittances.

- Submit this form to your HR or payroll department. Your employer is legally obligated to subtract the reported TCS amount from your total annual tax liability and proportionally reduce your remaining monthly TDS deductions.

Example

Suppose your total annual tax liability on your salary is ₹20,00,000. Without any adjustments, your employer deducts approximately ₹1,66,667 per month as TDS.

During the year, you remit ₹35 Lakhs to your global brokerage account. The first ₹10 Lakhs is exempt, and you pay a 20% TCS on the remaining ₹25 Lakhs, which equals ₹5,00,000 in TCS.

You submit Form 12BAA to your employer showing this ₹5,00,000 TCS credit. Your employer adjusts your annual tax liability down to ₹15,00,000. Your new monthly TDS becomes ₹1,25,000 or lower (depending on when you made the transaction and updated your employer). By doing this, you instantly free up at least ₹41,600 every month in your take-home pay instead of waiting for a refund next year.

For people engaged in business

Since you do not have an employer managing your tax deductions, you must execute this offset yourself during your standard quarterly advance tax calculations.

- Calculate your projected tax liability for the entire year based on your estimated business profits and other income.

- Deduct any tax that has already been withheld by your clients or customers.

- Deduct the total TCS you have paid on foreign investments, business software subscriptions, or international travel.

- The final resulting figure is your actual advance tax liability. You only pay this remaining balance in your scheduled installments.

Example

Suppose you are an independent contractor or freelancer and your estimated income tax liability for the year is ₹6,00,000.

You decide to invest heavily in global markets and remit ₹20 Lakhs. After the ₹10 Lakh exemption, you pay 20% TCS on the remaining ₹10 Lakhs, resulting in a TCS payment of ₹2,00,000.

When calculating your advance tax installments, you simply subtract the ₹2,00,000 TCS credit from your ₹6,00,000 liability. Your new net tax liability for the year is ₹4,00,000. You base your quarterly payments on this lower amount, immediately keeping ₹2,00,000 of working capital inside your business instead of locking it up with the government.

How Paasa helps with tax

Paasa is the platform used by global Indian Investors, NRIs, and family offices to diversify their wealth across global markets like US, UK, China, Singapore, Switzerland, and beyond.

Paasa offers a comprehensive advisory layer that keeps your portfolio compliant and makes tax filing hassle free with:

- Dedicated relationship manager

- Ongoing remittance, FEMA and tax advisory

- Ongoing tax loss harvesting and rebalancing

- End of year tax documents