The escalating technology confrontation between Washington and Beijing has turned semiconductor ETFs into a proxy battlefield for geopolitical risk.

Since October 2022, successive rounds of export controls have restricted China's access to advanced chips, manufacturing equipment, and the expertise needed to produce cutting-edge semiconductors. The controls now span 24 types of manufacturing equipment, high-bandwidth memory, and even prohibit U.S. persons from supporting certain Chinese fabrication facilities.

For investors holding semiconductor exposure through ETFs like SMH, SOXX, or XSD, these restrictions carry asymmetric consequences. The impact depends entirely on where a fund's holdings sit in the semiconductor value chain and how much revenue they derive from China.

Companies selling finished AI chips face different pressures than those manufacturing equipment or producing memory. The performance divergence between major semiconductor ETFs has widened meaningfully since export controls intensified.

Table of Contents

- The Concentration Question

- The Memory Wildcard

- Taiwan and Geographic Concentration

- Limits to the Analysis

- Investor Takeaway

The Concentration Question

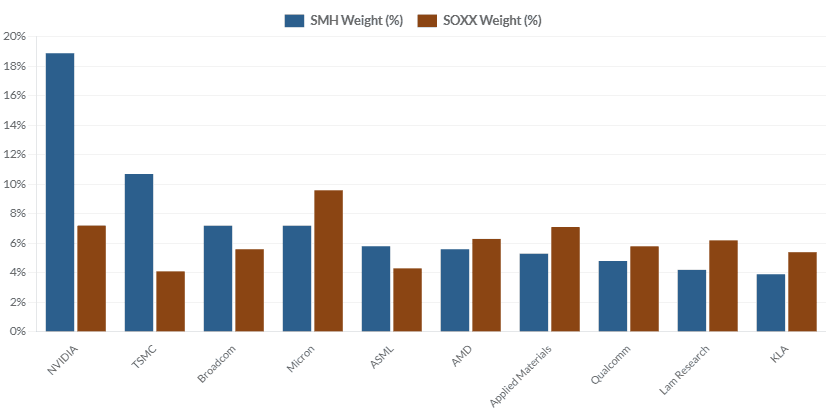

Portfolio construction determines everything in this environment. SMH holds 26 stocks with 76% of assets concentrated in its top 10 holdings.

NVIDIA alone accounts for nearly 19% of the fund. SOXX spreads exposure more evenly across 34 holdings, capping individual positions at roughly 10%. As the chart demonstrates, this structural difference creates dramatically different risk profiles.

The concentration story plays out in the weighting mechanics. In SMH, NVIDIA carries a 19% weight despite having a market capitalization 15 times larger than Applied Materials, which holds roughly 6%. The fund's modified market cap methodology allows individual positions to reach 20% before quarterly rebalancing intervenes. SOXX enforces stricter limits, capping the five largest holdings at 8% and all others at 4%. This produces a more balanced exposure but also dilutes upside when specific stocks surge.

Taiwan Semiconductor Manufacturing Company presents an interesting case. Despite a $1.5 trillion market value, TSMC holds only 4% in SMH due to ADR restrictions. The stock carries similar weight in SOXX. This structural constraint matters because TSMC sits at the geographic center of semiconductor geopolitical risk, producing 60% of the world's chips and 90% of the most advanced nodes entirely from Taiwan-based facilities.

The Memory Wildcard

While AI chip makers and equipment suppliers navigate export restrictions, memory producers face a different set of dynamics. Micron Technology holds the largest weight in SOXX at 9.6% and ranks fourth in SMH at 7.2%.

December 2024 controls added high-bandwidth memory to the restricted list, targeting HBM2E and above. This matters because advanced AI systems are memory-constrained, not just compute-constrained.

The controls aim to keep China at least two generations behind in HBM technology. Huawei's flagship AI processors still depend on Samsung-produced HBM2E, while SK Hynix and TSMC are planning HBM4 production by early 2025. For Micron, this creates both headwinds and tailwinds. Lost China sales in restricted categories reduce revenue, but tightening global HBM supply supports pricing power in unrestricted markets.

DRAM and NAND flash markets present additional complexity. Conventional memory products face less stringent controls than HBM, but China accounts for 35% of global semiconductor demand. Any broad deterioration in China's economic growth or technology investment directly impacts memory demand. At the same time, U.S. data center buildouts and AI infrastructure spending have created substitute demand that partly offsets China weakness.

Taiwan: The Geographic Concentration Nobody Can Diversify

TSMC's dominance introduces a risk that no amount of portfolio rebalancing can eliminate. The company fabricates chips for NVIDIA, AMD, Apple, Qualcomm, and virtually every other designer of advanced semiconductors. Any disruption to TSMC's Taiwan operations would cascade through the entire semiconductor ETF universe regardless of individual fund construction.

China faces similar geographic concentration risks, but in reverse. Over half of Taiwan's chip exports flow to China, creating a mutual dependence that theoretically restrains both sides.

However, if Beijing calculates that technology dominance justifies the economic cost of conflict, the restraining effect weakens. U.S. export controls may paradoxically reduce China's economic dependence on Taiwanese chips by forcing domestic substitution, potentially lowering Beijing's perceived threshold for military action.

Limits to the Analysis

Export control effectiveness depends on enforcement mechanisms that remain imperfect. Reports document smuggling operations moving hundreds of millions of dollars worth of restricted chips through third countries. A 2024 investigation uncovered a ring that purchased $390 million in servers containing banned NVIDIA GPUs, routing them through Malaysia via a company named "Luxuriate Your Life." Active markets in Shenzhen reportedly trade thousands of controlled chips. The volume of detected smuggling likely represents a fraction of total illicit flows.

China's response also introduces uncertainty beyond what revenue exposure data captures. Beijing has accelerated domestic chip development through massive subsidies, reportedly launching a $47.5 billion semiconductor investment fund in 2024.

Huawei's progress illustrates the challenge. After being cut off from U.S. technology in 2019, the company was expected to decline. Instead, by 2024 Huawei launched products featuring advanced semiconductors and developed 5G infrastructure, with SMIC reportedly producing chips designed by Huawei's HiSilicon subsidiary. Export controls may slow China's progress but won't prevent it entirely.

Investor Takeaway

Semiconductor ETF selection now requires weighing traditional factors like concentration and sector exposure against geopolitical risk that can't be diversified away.

SMH offers the purest play on AI infrastructure leaders but carries maximum exposure to both China revenue loss and Taiwan manufacturing concentration. SOXX provides more balanced exposure with modestly lower concentration risk, though the difference may not matter much if systemic shocks materialize. XSD spreads risk most evenly but sacrifices participation in the winners that have driven sector returns.

Investors convinced that AI infrastructure spending will continue to dominate semiconductor demand may accept SMH's concentration as the price of maximum upside capture. Those seeking to reduce single-stock and single-country risk while maintaining semiconductor exposure might prefer SOXX's structure.

And investors concerned that export controls will prove either ineffective or counterproductive, accelerating China's push for self-sufficiency while harming U.S. equipment makers, might reconsider semiconductor exposure altogether in favor of broader technology diversification.