If you are an Indian professional or businessperson who currently holds the Resident but Not Ordinarily Resident (RNOR) status and have foreign rental income, you might be confused about how India classifies and taxes this income.

This blog covers all you need to know about how India classifies foreign rental income for RNORs, when it is not taxed, and when it can be taxed by Indian authorities.

Table of contents

- Who is RNOR?

- What is foreign rental income?

- Is foreign rental income taxed in India?

- Can India classify it as income controlled from India?

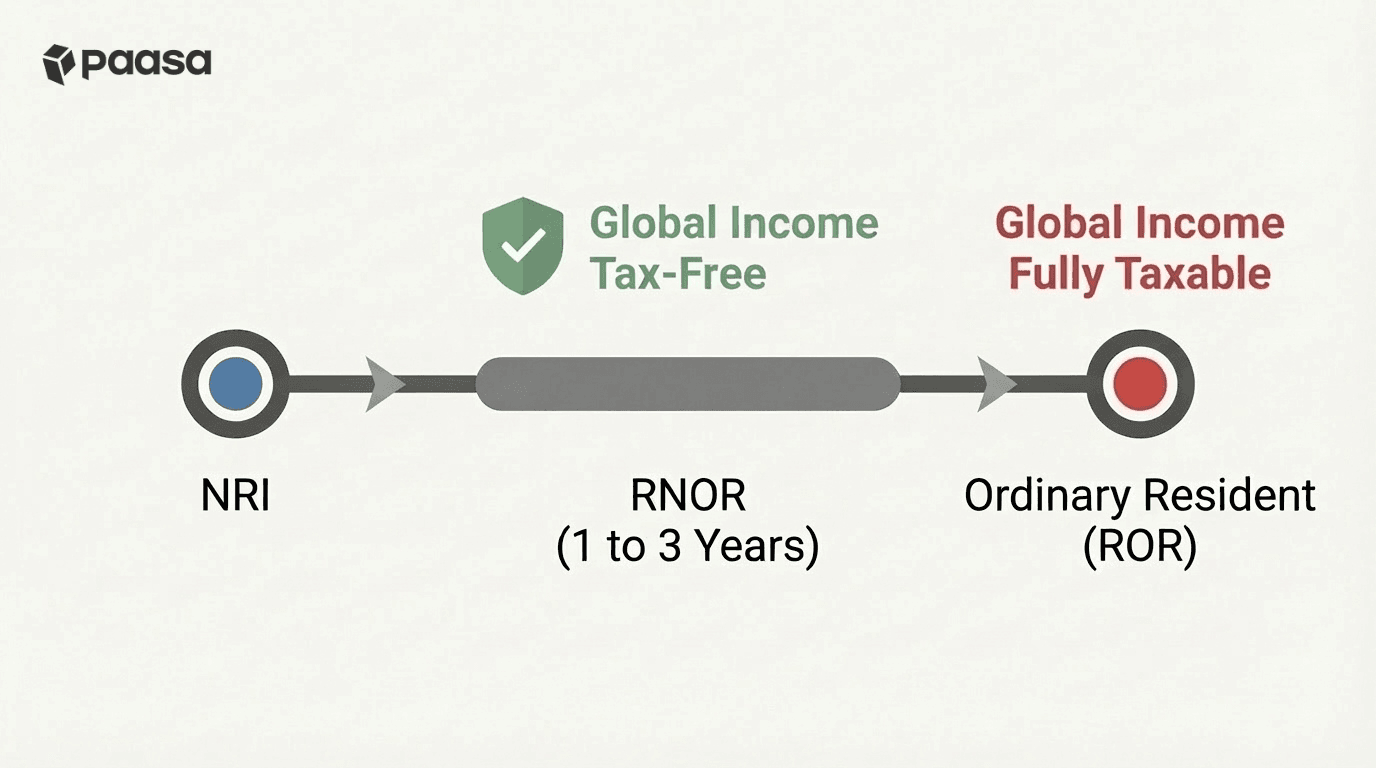

Who is considered RNOR?

To qualify as Resident but Not Ordinarily Resident, you must first be considered a "Resident" of India for the current year.

Once you are a Resident, you fall into the special RNOR category if you meet ANY ONE of the following criteria:

- You were a Non-Resident (NRI) in at least 9 out of the 10 financial years immediately preceding the current year.

- You were physically present in India for 729 days or less in total during the 7 financial years immediately preceding the current year.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

How long does it last?

The RNOR status can last from 1 to 3 years.

Most returning NRIs enjoy this status for 2 full financial years after the year they return. In some cases (depending on your arrival date), it can stretch to 3 years.

Once this period ends, you become an Ordinary Resident (ROR), and your global income becomes fully taxable in India.

What is considered foreign rental income in India?

If you have property located outside India generating rental income, the rent it generates is considered foreign income.

The classification depends entirely on the physical location of the asset, regardless of your citizenship or the currency of payment.

Examples

- Foreign Rental Income: You own a condo in Singapore or an apartment in the US. The rent is foreign income because the property is outside India.

- Indian Rental Income: You own a flat in Gurgaon and rent it to a US expat. This is Indian income because the property is inside India.

Is foreign rental income taxed in India when I am an RNOR?

For an RNOR, rental income from a property located outside India is tax-free in India.

This is because the Indian government considers this as income that "accrues or arises outside India." Since you are not a full Ordinary Resident yet, India does not claim a right to tax your global earnings, provided they are not derived from a business you control from India.

However, to keep this income tax-free, you must be careful about where you receive the money.

Receive it abroad first

To ensure the exemption, your tenant must deposit the rent into your foreign bank account (e.g., in the US, UK, or Singapore). Once the money hits your foreign account, the "income" is considered to have been received outside India.

After it is credited to your foreign account, you are free to transfer (remit) that money to your Indian bank account. This remittance is just a transfer of your own funds and is not taxable.

Do not receive it directly in India

If your tenant transfers the rent directly to your Indian bank account, it is treated as "income received in India." In this case, the exemption is lost, and the entire amount becomes fully taxable in India at your slab rate, even though the property is abroad and you are an RNOR.

Can there be a situation where India classifies it as income controlled from India and taxed accordingly?

The "business controlled from India" rule generally does not apply to rental income.

Here is why: Under Indian tax laws, income is classified into specific "heads." The "business controlled from India" clause applies only to income that falls under the head "Profits and Gains of Business or Profession."

Rental income falls under a completely different head: "Income from House Property."

Because your rental income is classified as "Property Income" and not "Business Income," the question of where it is controlled is legally irrelevant. Even if you sit in Mumbai and approve tenants or authorize repairs for your London flat, it remains "Property Income" and remains tax-free for an RNOR.

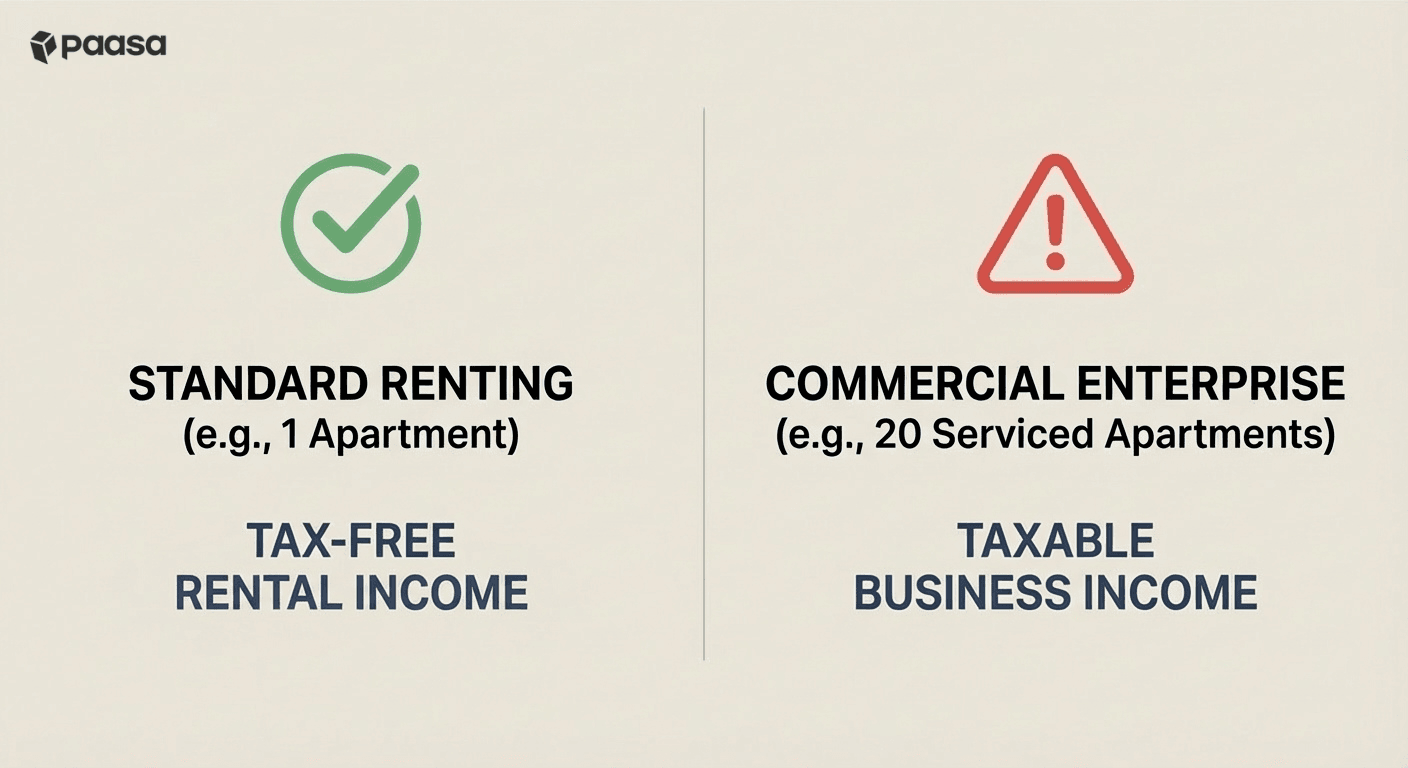

Exception

The only situation where this could be taxed is if your rental activity is so extensive that the Tax Department reclassifies it as a business.

Example:

You don't just own one house; you own 20 serviced apartments in Dubai. You have a team, you run daily operations, and you manage this entire commercial enterprise from your office in India.

In this specific case, the tax department could argue that you are not earning "rent" but running a "hotel business." If they reclassify your income as "Business Income," then the "Controlled from India" rule kicks in, and you would have to pay tax in India.

About Paasa

Transitioning your financial life back to India is complex. Paasa is designed to bridge that gap, acting as a single gateway for your global wealth while you settle back home.

- Keep Your Global Edge: No need to liquidate your overseas holdings. You get direct access to 10+ global exchanges (including the US, UK, JP, and SG) and can manage your wealth across 9 major currencies from one dashboard.

- FEMA & Tax Compliance Made Simple: Moving back means shifting from NRI to RNOR or RES status. We handle the heavy lifting by providing the exact reports required for Indian foreign asset disclosures (Schedule FA) and tax filings.

- No More Manual Calculations: Forget the nightmare of converting transaction history into INR for the IT Department. Our platform automates your tax reporting, so you stay compliant without the spreadsheets.

- Institutional-Grade Access: Whether you are looking at US Tech stocks or Swiss bonds, we provide the same high-level execution you were used to while living abroad, tailored for the Indian regulatory environment.