If you're an Indian professional working in companies like Microsoft, Apple, Google, etc, your employer stock grants can become a large part of your wealth over time as they vest and appreciate.

While RSUs can build wealth, they also create concentration risk. A large allocation to one company or sector means your portfolio depends heavily on its performance.

Deciding when and how to diversify is therefore an important part of managing your finances. This guide explains why concentration risk matters and how to reduce it effectively.

Table of Contents

- Why Concentration Risk Matters

- When Should You Start Diversifying Your RSUs?

- How to Reduce Concentration Risk

- Tax Considerations When Selling RSUs

- About Paasa

Why Concentration Risk Matters

Concentration risk occurs when a large portion of your portfolio is tied to a single asset, such as your employer's stock. For many employees, RSUs can grow into a significant part of their wealth over time, increasing reliance on one company's performance.

Concentration risk matters for these key reasons.

- Greater portfolio volatility: As your allocation to employer stock increases, your portfolio becomes more sensitive to movements in a single stock. This means changes in your company's share price can have a larger impact on your overall portfolio compared to a more diversified allocation.

- Double exposure to the same company: Your income, future RSU grants, bonuses, and investments may all depend on your employer. If the company underperforms, both your employment income and investment portfolio can be affected simultaneously.

For example, suppose your investment portfolio is worth $1,000,000 and 40% ($400,000) is invested in your employer's stock.

If your employer's share price falls by 30%, your employer stock would lose $120,000 in value, reducing your overall portfolio by 12%, even if all your other investments remained unchanged.

By comparison, if employer stock represented only 10% of your portfolio, the same decline would reduce your overall portfolio by just 3%.

Even if the broader market performs well, your portfolio can underperform simply because one company or one sector has performed poorly.

Why Concentration Matters for Estate Planning (US Estate Tax)

As your holdings grow, both your concentration risk and the value of your US-situs assets increase. This means a larger portion of your wealth is exposed not only to the performance of a single company but also to the potential impact of US estate tax.

For investors who have accumulated substantial holdings in US-listed company stock, US estate tax becomes another reason to diversify.

Unlike capital gains tax, which applies when you sell your shares, US estate tax applies if you pass away while still holding certain US-situs assets, including shares of US-listed companies.

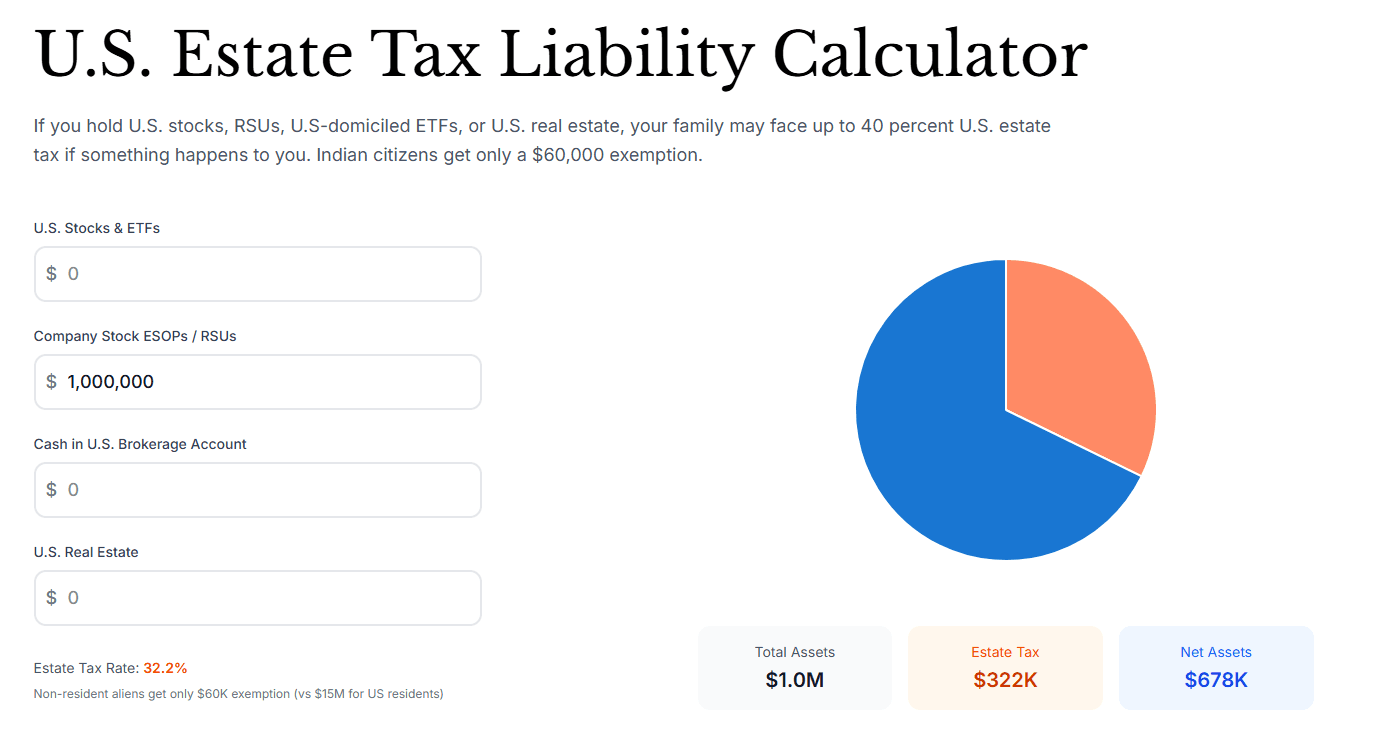

For non-US residents, only the first US$60,000 of US-situs assets is exempt. If the value of your US-situs assets exceeds this exemption at the time of death, the excess is subject to US estate tax under the applicable tax schedule, with the highest marginal rate reaching 40%.

Example

Suppose you are a software professional working in the US. Your total US assets, including stock market investments and other US-situs property, amount to $1,000,000.

In case you pass away, here is what your estate tax liability will look like:

- Gross US Estate: $1,000,000

- Less Exemption: ($60,000)

- Taxable Estate: $940,000

The tax is calculated progressively on this remaining $940,000.

In this scenario, out of your $1,000,000 hard-earned wealth, the IRS would take $322,000 before your family receives anything.

Use our Estate Tax Calculator to find your exact liability.

To learn how US estate tax is calculated in detail, read our guide on How US Estate Tax Works for Indians and NRIs.

When Should You Start Diversifying Your RSUs?

The right time to diversify depends on your overall financial situation, risk tolerance, investment goals, tax considerations, and your conviction in your company's long-term prospects.

Many investors begin reviewing their strategy when their employer's stock becomes a meaningful part of their portfolio, often around the 20-30% range.

It's also important to revisit your allocation whenever new RSUs vest, as your exposure can gradually increase over time.

If you've accumulated a substantial amount of US-listed company stock, consider diversifying once your US-situs assets begin approaching or exceed the US $60,000 estate tax exemption.

As your RSUs grow in value over time, reaching this threshold can be a practical point to reassess both your concentration risk and potential estate tax exposure, and decide whether to gradually reduce your position.

How to Reduce Concentration Risk

Reducing concentration risk is not about selling all your RSUs immediately. Instead, it is about gradually lowering your exposure to your employer's stock and reinvesting the proceeds into a more diversified portfolio.

This process involves two steps: selling shares systematically over time and using the proceeds to build a portfolio spread across different companies, sectors, and geographies.

Sell Your RSUs Systematically to Gradually Reduce Concentration Risk

Rather than selling all your shares at once, many investors choose to reduce their exposure gradually over multiple vesting cycles. Instead of trying to predict the best time to sell, a systematic approach helps you follow a consistent framework that is aligned with your long-term financial goals.

It can also reduce the influence of short-term market movements and emotional decision-making while steadily bringing your employer stock allocation closer to your target.

Some common approaches include:

- Sell a fixed percentage at every vesting event. For example, you might decide to sell 50% or 75% of every RSU vest as soon as it becomes available. This helps reduce your employer stock exposure consistently while still allowing you to retain some shares.

- Maintain a target allocation to employer stock. Decide what percentage of your overall investment portfolio you're comfortable keeping in your employer's stock. Whenever your allocation exceeds that target, sell enough shares to bring it back in line.

- Spread sales throughout the year. Instead of making one large sale, you can sell smaller amounts periodically over the course of the year. This helps reduce market timing risk and can make your selling strategy more disciplined.

The right approach depends on your financial goals, tax situation, and overall investment strategy. Since taxes can significantly affect your net returns, it's important to understand how RSUs are taxed at every stage.

For a step-by-step framework to help you evaluate these factors and decide when to sell, read our How to Sell RSUs: A Practical Framework for Deciding When to Sell guide.

To understand the full RSU taxation lifecycle from grant to sale, read our guide on RSU Taxation Explained: From Grant and Vesting to Sale

Reinvest the Proceeds Into a Diversified Portfolio

Selling your employer's stock is only one part of reducing concentration risk. The next step is reinvesting the proceeds into assets that provide broader diversification.

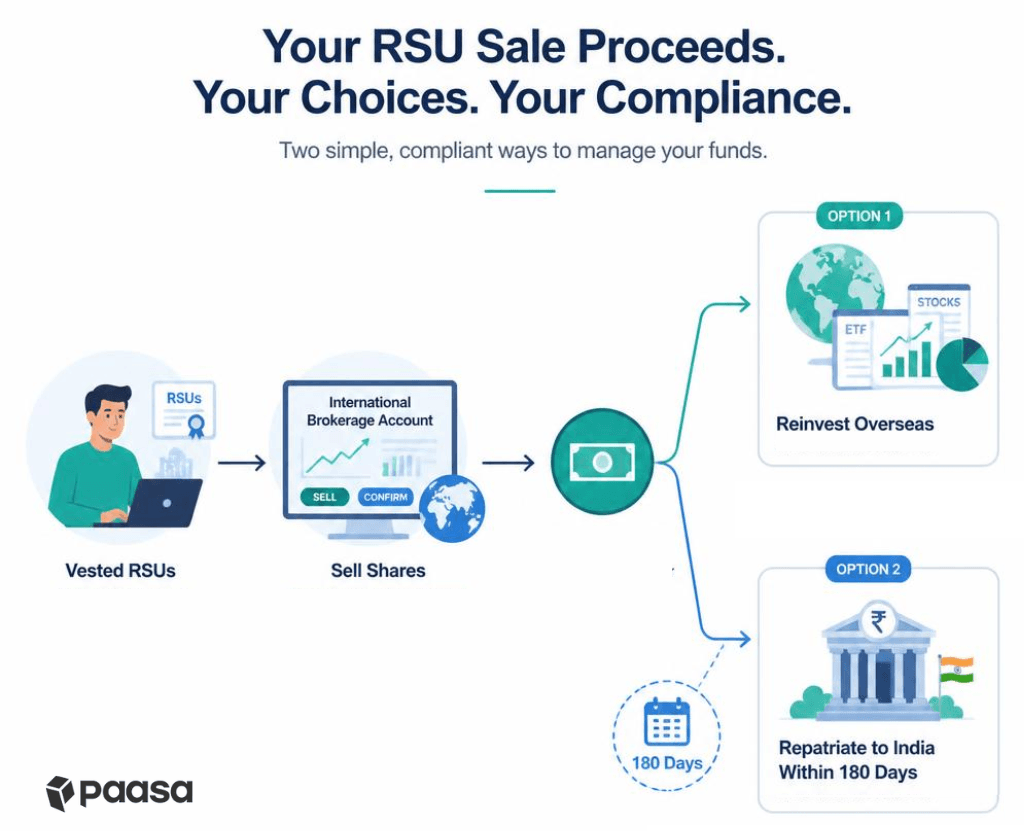

Before selling your RSUs, it's worth considering how you'll reinvest the proceeds. Under FEMA, vested RSUs are treated as Overseas Portfolio Investments (OPI), which means the proceeds from selling your shares must either be reinvested overseas or repatriated to India within 180 days.

Planning how you'll deploy these funds before selling can help you remain compliant while avoiding idle cash.

To understand how the 180-day rule works and what it means for RSU investors, read our guide on FEMA 180-Day Rule for Overseas Investments.

Depending on your investment strategy, this may include:

- Broad-market ETFs that provide exposure to hundreds or thousands of companies through a single investment.

- Sector ETFs to diversify your portfolio across industries rather than remaining heavily invested in your employer's sector.

- Direct stocks that provide exposure to companies across different sectors and industries, helping reduce concentration in your employer's stock.

- Other asset classes, such as bonds or fixed-income investments, depending on your financial goals and risk tolerance.

The objective is not to eliminate risk entirely, but to avoid having a large portion of your wealth depend on the performance of one company.

Use UCITS ETFs to Build a Globally Diversified Portfolio

For investors seeking long-term international exposure, Ireland-domiciled UCITS ETFs provide broad diversification while helping reduce US estate tax exposure compared with holding US-listed securities directly.

They are commonly used by Indian investors to gain global market exposure, as they offer lower dividend withholding tax (15%), no US estate tax exposure, and accumulating share classes that automatically reinvest dividends.

How Paasa Can Help

Paasa helps Indian investors and RSU holders access global markets with ease, enabling investments across the US, Europe, China, Japan, and other major economies.

Trusted by HNIs, family offices, and institutions, Paasa combines international investing opportunities with India-focused support and compliance.

Paasa helps you hold and protect your RSU wealth with:

- In-kind transfer from your existing brokerage account

- Access to US, Europe, China, Japan, and other major economies

- Access to UCITS ETFs that protect against the US estate tax risk

- Comprehensive tax reporting tailored for Indian investors, including capital gains, dividend taxation, and TCS tracking.