NRIs returning to India are often confused about their tax residency status in India in the year they are returning and a few years after that.

This blog covers all three Indian tax residency statuses, Resident Ordinarily Resident (ROR), Resident but Not Ordinarily Resident (RNOR), and Non-Resident (NR); and the rules that determine your classification into them.

Table of contents

- Who is considered Resident (ROR)?

- Who is considered Non-Resident (NR)?

- Who is considered RNOR?

- Determining RNOR status

- Tax liabilities changes during transition

Who is considered a resident (ROR) in India?

To be considered a Resident for tax purposes in any financial year (April 1 to March 31), you must meet specific conditions related to your physical presence or citizenship.

1. The Basic Physical Presence Tests

You are a Resident if you meet ANY ONE of the following criteria:

- The 182-Day Rule: You are in India for 182 days or more during the financial year.

- The 60 + 365 Rule: You are in India for 60 days or more during the year AND have been in India for 365 days or more in the preceding 4 years.

2. Special Exceptions for Indian Citizens & PIOs

The "60-day" threshold mentioned above changes in specific cases:

- Leaving for Employment: If you are an Indian citizen leaving India for employment or as crew on an Indian ship, the 60 days are replaced by 182 days.

- Visiting India: If you are an Indian citizen or Person of Indian Origin (PIO) visiting India:

- Generally, you only become a resident if you stay for 182 days or more.

- However, if your total income (excluding foreign sources) exceeds ₹15 Lakhs, you become a resident if you stay for 120 days or more (provided you also meet the 365-day rule).

3. Deemed Residency (Citizens with No Tax Home)

You are legally "Deemed to be Resident" in India, even if you don't meet the physical presence tests above, if you meet ALL three conditions:

- You are an Indian Citizen.

- Your total income (excluding foreign sources) exceeds ₹15 Lakhs.

- You are not liable to tax in any other country or territory by reason of your domicile or residence.

If you meet any of these definitions, you are a Resident. You will then be classified as an "Ordinary Resident (ROR)" unless you qualify for the specific "RNOR" exemptions discussed next.

Who is considered a non-resident (NR) in India?

If you do not meet the criteria to be a "Resident" (as defined in the previous section), you are automatically classified as a Non-Resident (NR).

Generally, you are an NR if:

- You were physically present in India for less than 60 days during the financial year.

- OR

- You were present for 60 to 181 days, but you spent less than 365 days in India during the preceding 4 years.

Who is considered an RNOR in India?

To qualify as an RNOR (Resident but Not Ordinarily Resident), you must first meet the criteria to be a "Resident" in the current financial year.

Once you are a Resident, you are classified as an RNOR if you meet ANY ONE of the following conditions:

1. Past Non-Residency Test

You were a Non-Resident in India in at least 9 out of the 10 tax years preceding the current year.

2. 729 Days Test

You were physically present in India for 729 days or less in total during the 7 tax years preceding the current year.

3. 120-Day Rule

You are an Indian Citizen or Person of Indian Origin (PIO) who:

- Has total income (excluding foreign sources) exceeding ₹15 Lakhs; AND

- Stayed in India for 120 days or more but less than 182 days during the year.

4. Deemed Resident Rule

You are an Indian Citizen who is "Deemed to be Resident" (because your Indian income exceeds ₹15 Lakhs and you are not liable to tax in any other country).

Tax Liability for RNOR

- Income earned in India: Taxable.

- Income earned abroad (Foreign Income): Tax-Free, provided it is not derived from a business controlled in or a profession set up in India.

How can I find out if I am considered RNOR in this financial year?

Determining your status in India can be confusing because it involves looking at your history over the last 10 years. To make it simple, follow this two-step check.

Step 1

First, ask yourself: "Am I a Resident of India this year?"

- NO: If you spent less than 60 days in India, you are likely still a Non-Resident (NRI). You do not need to check for RNOR.

- YES: If you are a Resident, proceed to Step 2.

Step 2

If you passed Step 1, you are a Resident. Now, check if you fall into the special "Not Ordinarily Resident" category.

Answer these two questions about your history before the current financial year starts.

| Question | Answer | Implication |

|---|---|---|

| 1. Were you an NRI in at least 9 out of the last 10 financial years? | YES | You are RNOR. |

| 2. Was your total stay in India 729 days or less in the last 7 financial years? | YES | You are RNOR. |

The Result:

- If the answer to EITHER question is YES, you are RNOR.

- If the answer to BOTH questions is NO, you are an Ordinary Resident (ROR) and your global income is fully taxable.

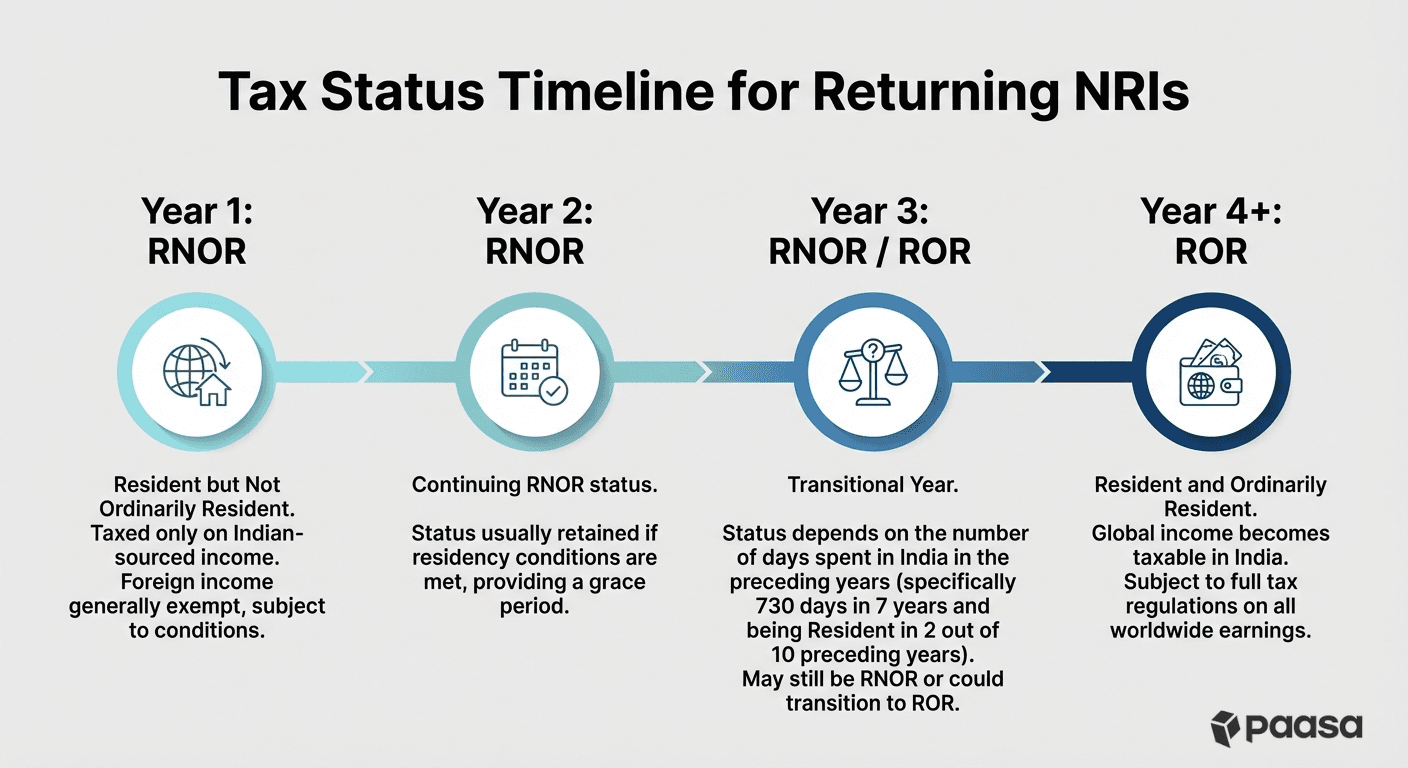

Rule of Thumb for Returning NRIs

If you have lived abroad for a long time (e.g., 5+ years) and have just moved back to India permanently:

- Year 1 (Year of Return): You are likely RNOR (or NRI, depending on the month you arrived).

- Year 2: You are almost certainly RNOR.

- Year 3: You might still be RNOR (depending on your exact arrival date).

- Year 4 onwards: You typically become an Ordinary Resident (ROR).

Important Note:

The steps above provide a general framework applicable to most returning NRIs. However, tax residency rules can become complex depending on your travel history and global income structures. This guide is not a comprehensive legal determination for every scenario. We strongly recommend consulting a qualified professional to confirm your exact residential status before making financial decisions.

Example

Suppose you are a software engineer who lived in the US for 8 years (2017–2025). You decided to move back to India permanently and landed in Bangalore on July 1, 2025.

Here is how your tax status changes over the next few years.

Year 1: Financial Year 2025-26 (The Year of Return)

- Physical Presence in India: ~274 days (July 1, 2025 – March 31, 2026).

- Status: Resident.

- Reason: You spent more than 182 days in India, so you pass the basic residency test.

- Sub-Status: RNOR.

- Reason: You pass the "729 Days Rule". We look at the 7 preceding years (2018–2025). Since you were living in the US during this entire period, your total stay in India was likely just a few weeks of vacation, far below the 729-day limit.

- (Note: You do NOT pass the "9 out of 10" test because you were only NRI for 8 years, but passing one test is sufficient).

- Tax Impact: Your US income and capital gains remain tax-free in India.

Year 2: Financial Year 2026-27

- Physical Presence in India: 365 days (Full year).

- Status: Resident.

- Sub-Status: RNOR.

- Stay in FY 2025-26: 274 days.

- Stay in previous years: ~0 days.

- Total: ~274 days.

- Since 274 is less than 730, you are still RNOR.

- Tax Impact: Global income remains tax-free.

Year 3: Financial Year 2027-28

- Physical Presence in India: 366 days (Leap year).

- Status: Resident.

- Sub-Status: RNOR.

- Stay in FY 2026-27: 365 days.

- Stay in FY 2025-26: 274 days.

- Total: 639 days.

- Since 639 is still less than 730, you remain RNOR.

- Tax Impact: Global income remains tax-free.

Year 4: Financial Year 2028-29

- Status: Ordinary Resident (ROR).

- Reason: We check the "729 Days Rule" for the preceding 7 years.

- Total stay = 366 (Year 3) + 365 (Year 2) + 274 (Year 1) = 1,005 days.

- Since 1,005 is greater than 730, you fail the RNOR test.

- Tax Impact: You are now an Ordinary Resident. Your entire global income is fully taxable in India, and you must report all foreign assets in Schedule FA.

How does my tax liabilities in India change when I transition from Non-Resident → RNOR → Resident?

As you transition from Non-Resident (NR) to RNOR and finally to Ordinary Resident (ROR), the scope of income that India can tax expands significantly.

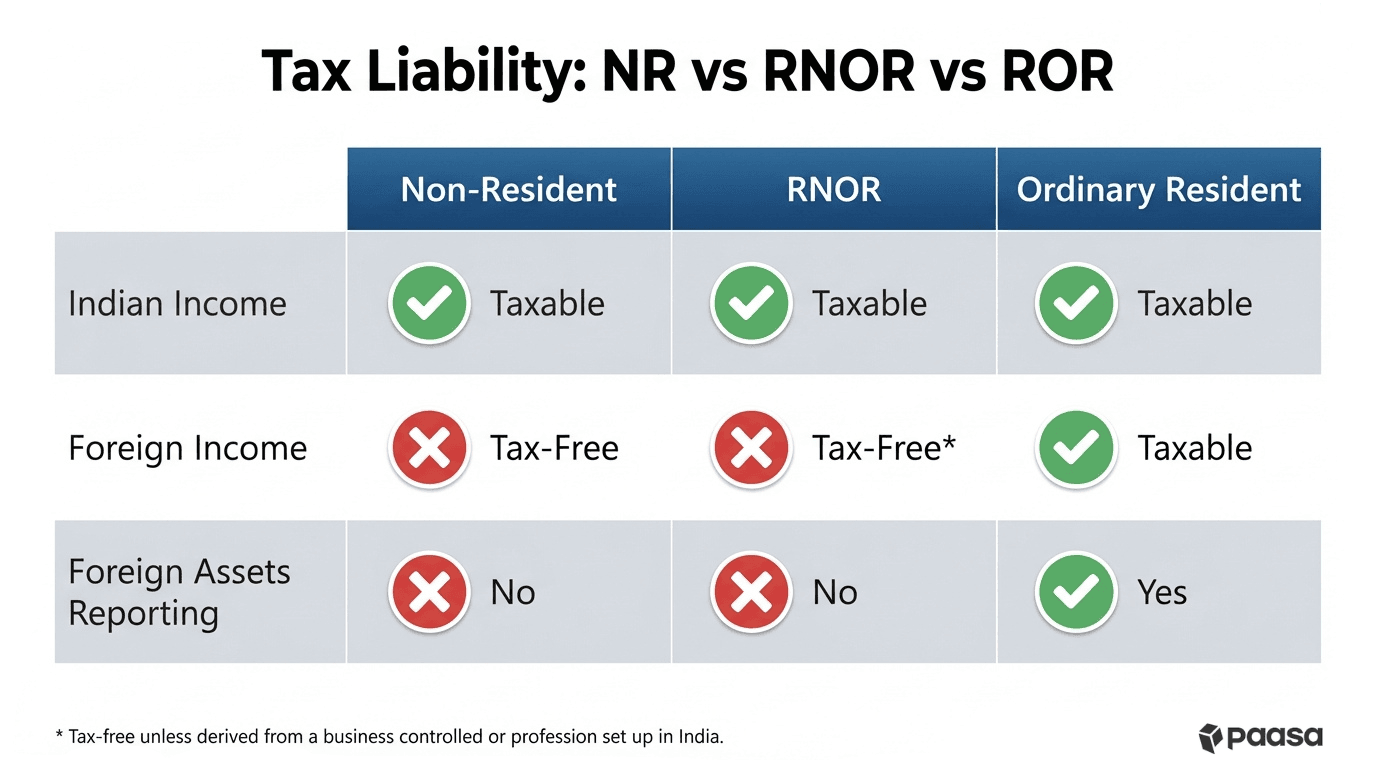

1. Non-Resident (NR)

Taxable only on Indian income.

You are taxed only on income that is earned, accrued, or received in India. This includes your salary for services rendered in India, rental income from Indian property, or interest from Indian savings accounts. Your foreign income (like US salary or dividends) is completely tax-free in India.

2. RNOR (Transitional Status)

Taxable on Indian income + controlled foreign income.

You are taxed on all Indian income, just like an NR.

However, your foreign income remains tax-free, with one rare exception: foreign income derived from a business controlled in India or a profession set up in India is taxable.

For most individuals with passive income (stocks, rent) abroad, this status is effectively the same as being an NR.

3. Ordinary Resident (ROR)

Taxable on global income.

You are taxed on your entire global income.

This includes all income earned in India and all income earned anywhere else in the world. You must report and pay tax on foreign salary, dividends, interest, and rental income.

You also have mandatory reporting requirements for all foreign assets (Schedule FA).

Comparison of Tax Liability by Status

| Non-Resident (NR) | RNOR (Transitional) | Ordinary Resident (ROR) | |

|---|---|---|---|

| Indian Income | Taxable | Taxable | Taxable |

| Foreign Income | Tax-Free | Tax-Free (Unless derived from a business controlled in India) | Taxable (Taxed in India at your slab rate) |

| Foreign Assets Reporting | Not Required | Not Required | Mandatory (Must declare all foreign bank accounts, stocks, and properties) |

| Global Income Tax | No | No | Yes |

What happens when you become an Ordinary Resident (ROR)?

The most significant change occurs when your RNOR status expires and you become an Ordinary Resident (ROR).

1. Your Global Income becomes Taxable

As an RNOR, you are not taxed on foreign income (like US dividends or interest).

Once you become an ROR, this advantage ends. You must report all foreign income in India, convert it to INR, and pay tax on it at your applicable slab rate.

You can claim a credit for taxes paid abroad, but the income is fully taxed as per Indian tax regulations.

2. Mandatory Reporting of Foreign Assets (Schedule FA)

- As an RNOR: You are not required to disclose your foreign assets to Indian tax authorities.

- As an ROR: You MUST file "Schedule FA" (Foreign Assets) in your Income Tax Return. You are legally required to list every foreign bank account, brokerage account, and property you own, even if they generated zero income. Failure to do so can attract severe penalties under the Black Money Act.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore and support 9 global currencies.

- Seamless "In-Kind" Transfers (ACATS): You can move your entire US stock portfolio (from brokers like Robinhood, Schwab, Fidelity, E*TRADE, and more) directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents.