Indian professionals who are moving back from the US often lack clarity about how they can manage their overseas holdings like stocks, ETFs, 401k accounts, and RSUs after moving back.

This article explains how you can manage your overseas holdings after moving back to India, and the Indian tax and reporting requirements you will be subject to. We also cover your tax residency status, how it changes, how you can avoid double taxation, and RNOR rules and opportunities.

Table of contents

- What happens to my stocks when I move back to India?

- What happens to my RSUs and stock options when I move back?

- What happens to my 401k when I move back to India?

- What happens to my IRA when I move back to India?

- What happens to my US property when I move back?

- Tax and reporting implications of moving back to India

- What is RNOR status and how does it affect me?

- Common Questions US NRIs Have About Moving Back

- About Paasa

What happens to my stocks when I move back to India?

Most US brokerage firms are designed to serve US residents. When you move back to India, you become a "Non-Resident Alien" (NRA) in the eyes of the US tax system, and many brokers do not support NRA accounts.

Here is how different platforms typically handle the move:

- Robinhood, Webull, M1 Finance: These platforms do not support non-US residents. If they detect a foreign IP address or if you update your address to India, they may restrict your account or force you to liquidate your positions immediately.

- Schwab, Fidelity, E*TRADE: These brokers are more flexible and usually allow you to convert your account to an International account. However, you will likely face restrictions: you may lose access to US Mutual Funds, dividend reinvestment plans (DRIP) might be disabled, and you will have to manage complex tax reporting manually. They also have high withdrawal charges and poor FX rates.

What's the best way to stay invested globally after moving back to India?

The best way to stay invested globally after moving back to India is transferring your investments into a platform that is specifically made for global investing from India.

These platforms will allow you to maintain your positions and trade as usual, while providing India specific compliance support like filing form W-8BEN and tax documents tailored for indian reporting requirements.

“Do not need to sell your stocks just because you are moving. Selling triggers a taxable event. Instead, use an ACATS transfer (Automated Customer Account Transfer Service). This allows you to move your entire portfolio "in-kind" (as is) to an India-friendly platform like Paasa.“

What happens to my RSUs and stock options when I move back?

If you worked at a US company, you likely have Restricted Stock Units (RSUs), Incentive Stock Options (ISOs), or Non-Qualified Stock Options (NQSOs) as part of your compensation. Each of these is handled differently when you leave the US.

RSUs

When an RSU vests, the IRS treats it as ordinary income equal to the fair market value of the shares on the vesting date. This is reported on your W-2 and subject to US income tax withholding, regardless of where you live at the time.

What happens to unvested RSUs when you leave your US employer depends entirely on your equity plan documents:

- Most plans forfeit unvested RSUs upon resignation. You walk away from them.

- Some plans offer accelerated vesting as part of an exit negotiation, particularly for senior employees.

- A few plans allow a post-termination exercise window, typically 30 to 90 days.

Check your equity plan documents or ask your HR team before confirming your resignation date.

Tax treatment during RNOR

If your RSUs vest after you have returned to India and when you have RNOR status, the income is still classified as US-source income (it was earned while you were working in the US). This means:

- The US will withhold tax as usual at the time of vesting.

- India will not tax this income during your RNOR window, since foreign income is exempt during this period.

Your cost basis in the shares becomes the fair market value at the time of vesting. Any gains from selling after that point are calculated from this basis.

ISOs and NQSOs

Non-Qualified Stock Options (NQSOs) are taxed as ordinary income at exercise, just like RSUs. Incentive Stock Options (ISOs) are more complex: they are not taxed at exercise for regular income tax purposes, but the spread can trigger the Alternative Minimum Tax (AMT). If you hold ISOs and are planning to return, consult a US tax advisor before exercising, as the AMT exposure can be significant.

Note: The tax treatment of RSUs that straddle your period of US and India residency (partly earned in the US, partly in India) can be complex. India and the US apportion income based on the number of workdays in each country during the vesting period. Keep records of your travel and work history.

What happens to my 401k when I move back to India?

A common misconception is that you must close your 401(k) or sell your investments when you leave the US. This is incorrect.

Your 401(k) is legally yours, regardless of where you live. You can continue to hold it, manage the investments within it, and eventually withdraw from it in retirement, even if you never return to the US.

However, once you leave your job, you generally cannot make new contributions to that specific plan. Your account essentially goes into "maintenance mode"—the funds stay invested and continue to grow tax-deferred.

Should I withdraw my 401k or keep it as-is?

You can either withdraw your 401k (and pay a 10% penalty plus taxes) or keep is as is when moving back to India. Here are the pros and cons of each option:

1. Leave it

If your account balance is over $7,000, most plan administrators allow you to keep the funds in the existing plan indefinitely.

In this case, your money continues to grow, and you can withdraw it without paying the 10% penalty after you turn 59.5 years old.

- Estate Tax Risk: If you pass away while holding more than $60,000 in US assets (including your 401k) as a non-resident, your estate will be subject to an up to 40% US Estate Tax. This is a risk you will have to take if you decide to leave your 401k as-is.

2. Withdraw the Funds

You can choose to liquidate the account.

If you do this before age 59½, you will face a flat 10% early withdrawal penalty on top of the standard US income tax applicable to that amount.

Despite the penalty, this option gives you the freedom to invest the money where you want.

It also allows you to avoid the US Estate Tax. By taking the cash out and reinvesting it in "Non-US Situs" assets , you ensure your heirs are not hit with the 40% tax on that wealth.

Note: There is no single "best" answer here. Leaving the money allows for tax-deferred growth but carries estate tax risks. Withdrawing it incurs an immediate cost but offers freedom and safety from future US taxes. The right strategy depends entirely on your specific financial goals and risk tolerance.

To learn more about the US Estate Tax risk, read our detailed guide on the US Estate Tax.

What happens to my IRA when I move back to India?

Many US professionals hold Individual Retirement Accounts (IRAs) in addition to their 401(k). The two most common types are the Traditional IRA and the Roth IRA, and they behave differently once you leave the US.

Should I roll over my 401(k) into an IRA before leaving?

Rolling over your 401(k) into a Traditional IRA is a standard move many financial advisors recommend when leaving a job. It consolidates your retirement savings, gives you more control over your investment choices, and removes you from dependence on your former employer's plan administrator.

A direct rollover (where funds move from your 401(k) custodian directly to an IRA custodian) is not a taxable event. No penalties apply. If you go this route, make sure the rollover is direct to avoid the mandatory 20% withholding that applies to indirect rollovers.

Traditional IRA

A Traditional IRA works similarly to a 401(k) once you are outside the US. You cannot make new contributions once you no longer have US earned income.

The funds continue to grow tax-deferred, and withdrawals after age 59½ are subject to US income tax.

Under Article 20 of the India-US DTAA, retirement income from US pension plans is generally taxable only in the country of residence. This means that when you become a full Resident and Ordinarily Resident (ROR) in India, your Traditional IRA withdrawals may be taxable in India rather than the US.

Roth IRA

The Roth IRA is the more complicated case. In the US, qualified Roth withdrawals are completely tax-free because contributions were made with post-tax dollars. However, India does not have an equivalent account structure, and the India-US DTAA does not explicitly address Roth IRAs.

This creates a practical risk: once you become a full ROR in India, the Indian tax authorities may treat Roth withdrawals as ordinary foreign income, subjecting them to Indian income tax, even though you already paid tax on the contributions in the US.

During your RNOR window, this is not an issue since foreign income is exempt. The problem arises when you become ROR.

Note: There is no definitive CBDT ruling or DTAA clarification on the Indian tax treatment of Roth IRA withdrawals. You should consult a cross-border tax expert before your RNOR status expires.

| Account Type | New Contributions After Return | Growth | Withdrawal Tax (US) | Withdrawal Tax (India, as ROR) |

|---|---|---|---|---|

| 401(k) | Not possible | Tax-deferred | Yes, as ordinary income | Likely exempt under DTAA Art. 20 |

| Traditional IRA | Not possible (no US earned income) | Tax-deferred | Yes, as ordinary income | Likely exempt under DTAA Art. 20 |

| Roth IRA | Not possible (no US earned income) | Tax-free | Tax-free in US | Unclear, seek advice |

What happens to my US property when I move back?

US real estate is excluded from most departure-related tax events. There is no US exit tax on property when you leave. You can continue to hold it indefinitely. However, two separate obligations apply once you become a non-resident: rental income is taxed differently, and selling triggers the FIRPTA withholding mechanism.

Rental income as a non-resident

If you rent out your US property after returning to India, the rental income is taxable in the US. As a non-resident alien (NRA), the default treatment is a flat 30% withholding tax on gross rental income with no deductions allowed. Your tenant or property manager is technically the withholding agent.

Most returning NRIs choose to make the IRC Section 871(d) net election instead. This election treats your US rental income as effectively connected income, which means you pay US tax at graduated rates on your net income after deducting allowable expenses such as mortgage interest, property management fees, depreciation, repairs, and property taxes. You must then file a Form 1040-NR each year to report this income. This is almost always more tax-efficient than the 30% gross withholding route, especially for properties with significant expenses.

How does India treat this rental income?

This depends on your Indian residency status:

- During RNOR: Rental income from your US property is tax-free in India, provided it is received in your US bank account first. If it is wired directly to an Indian account, it is treated as received in India and becomes taxable immediately. Read our guide on foreign rental income for RNORs for the full treatment.

- After becoming ROR: India also taxes the rental income at your applicable slab rate. Under Article 6 of the India-US DTAA, rental income from immovable property is taxable in the country where the property is located. The US retains primary taxing rights. India gives you a foreign tax credit for the US tax already paid, so you pay the difference rather than the full amount twice.

Example

You rent your California property for $4,000 per month ($48,000 per year). Your allowable deductions are $18,000. You have made the IRC 871(d) net election. You are in the 30% Indian slab with income above ₹2 crore.

| Component | RNOR year | ROR year |

|---|---|---|

| Gross rental income | $48,000 | $48,000 |

| Allowable US deductions | $18,000 | $18,000 |

| US taxable income (A) | $30,000 | $30,000 |

| US federal tax at ~22% on (A) (B) | ~$6,600 | ~$6,600 |

| Indian base tax at 30% on gross (C) | Nil | $14,400 |

| Surcharge at 25% of (C) (D) | Nil | $3,600 |

| Cess at 4% of (C+D) (E) | Nil | $720 |

| Gross Indian tax (C+D+E) (F) | Nil | $18,720 |

| Foreign tax credit for (B) (G) | N/A | $6,600 |

| Net Indian tax payable (F minus G) | Nil | $12,120 |

| Total tax paid | ~$6,600 | ~$18,720 |

Note: State income tax applies separately on US rental income depending on the state your property is in. California, for example, taxes non-resident rental income at its standard rates. Factor your state liability into the comparison above.

Selling US property as a non-resident

When you sell US property as a non-resident, the buyer is required to withhold 15% of the gross sale price under the Foreign Investment in Real Property Tax Act (FIRPTA) and remit it to the IRS. This withholding is on the full sale price, not your gain. You recover any excess by filing a US tax return for the year of sale.

The one exception: If the buyer is purchasing the property as their personal residence and the sale price is $300,000 or less, FIRPTA withholding does not apply. This exception is buyer-specific and requires the buyer to intend to use the property as a residence.

Reducing the withholding with Form 8288-B

If your actual US capital gains tax liability is lower than 15% of the gross sale price, which is common when the property has a high purchase price relative to the gain, you can apply for a withholding certificate using Form 8288-B before or on the date of sale. The IRS will assess your actual liability and issue a certificate allowing the buyer to withhold at a reduced rate. Apply well before closing, as processing takes time and the sale cannot close at the reduced rate without the certificate in hand.

Which country taxes the gain, and when?

Under Article 13 of the India-US DTAA, the US has primary taxing rights on gains from US real property regardless of where you live. India also retains the right to tax as your country of residence once you are a full ROR.

- During RNOR: The gain is completely exempt in India. Only the US taxes the sale. This is the most efficient window to sell.

- After becoming ROR: India taxes the gain as long-term capital gains at 12.5% without indexation (for property held over 24 months, under post-2024 budget rules). India gives you a foreign tax credit for the US federal capital gains tax already paid. If you fall in the US federal long-term capital gains rate of 15% or 20%, it exceeds India's 12.5%, meaning no additional Indian tax is owed in practice after the credit.

Note: US long-term capital gains rates for non-resident aliens are 0%, 15%, or 20% depending on the amount of gain. Additionally, if you have claimed depreciation on the property during the rental period, a portion of the gain attributable to depreciation is taxed at 25% (unrecaptured Section 1250 gain) rather than the standard long-term rate. Factor this in when estimating your US liability.

A note on US state taxes

Federal taxes are only part of the picture. If you lived in California or New York, your state tax obligations do not automatically end when you board the flight back to India.

California

The California Franchise Tax Board (FTB) uses a domicile-based residency test. For a detailed breakdown of how California determines residency, refer to FTB Publication 1031.

If California remains your "domicile" (the place you intend to return to), the FTB can continue to tax your worldwide income even after you physically leave. California is known for auditing high-income individuals who claim to have left.

To establish non-residency before leaving, you need to take concrete steps: update your voter registration, surrender your California driver's licence, close California-based bank accounts where possible, and file a part-year resident return for the year of departure. Simply moving is not enough.

New York

New York uses both a domicile test and a statutory residency test.

If you maintain a permanent place of abode in New York and spend more than 183 days in the state in a calendar year, New York can tax you as a resident regardless of where you claim to be domiciled.

Note: If you lived in California or New York and have significant investment income (dividends, capital gains, 401(k) withdrawals), confirm your departure is properly documented with the relevant state tax authority or a US CPA before you leave.

Tax and reporting implications of moving back to India

When you permanently return to India, your tax status eventually shifts from being a Non-Resident Indian (NRI) to a Resident.

This brings two major changes: your global income becomes taxable in India, and your reporting requirements increase significantly.

To learn more about how your global income is taxed in India and the reporting requirements, read:

- How Global Stocks and ETFs Are Taxed for Indian Investors

- Tax on Repatriation of Foreign Income to India

- Foreign Asset Disclosure (Schedule FA) Requirements for Indians

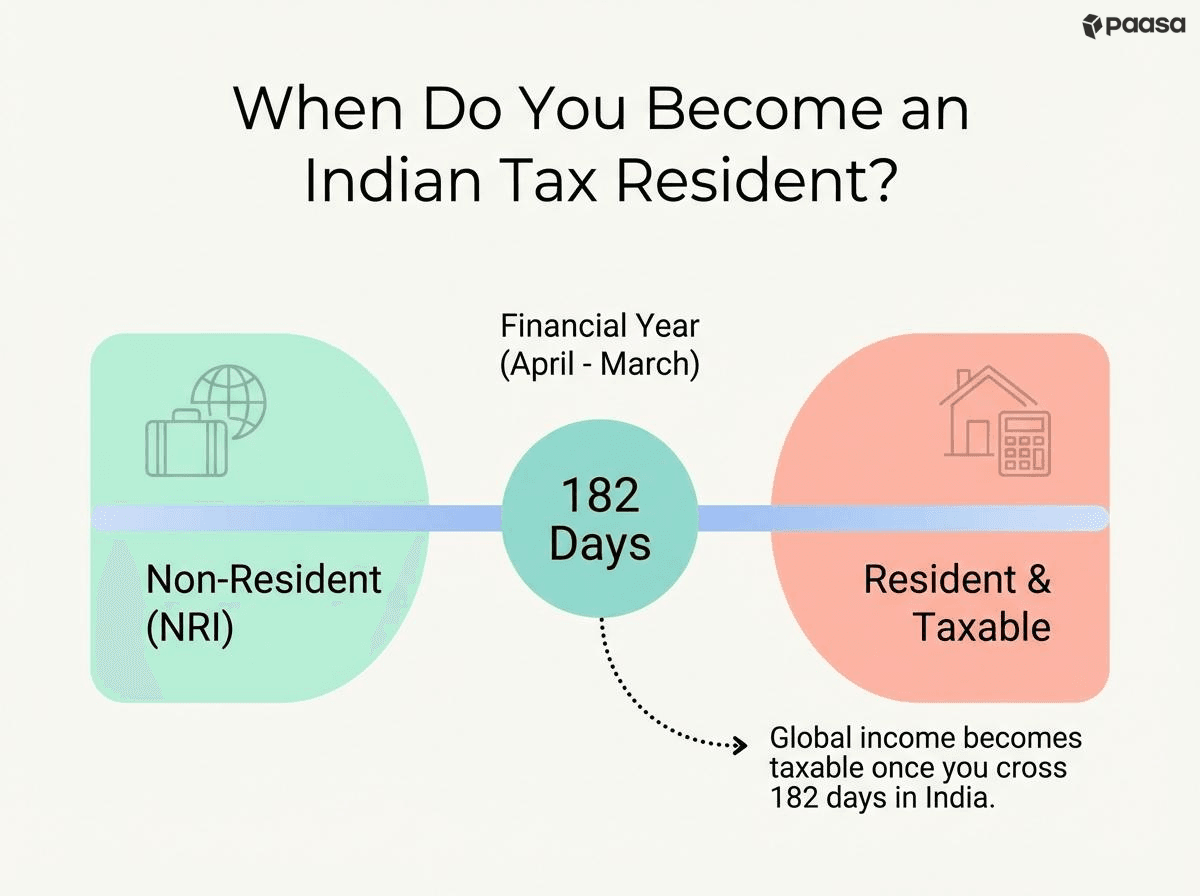

When do you become a Tax Resident?

Under the Income Tax Act, You are considered a tax resident of India if:

- You are physically present in India for a period of 182 days or more in the tax year (182-day rule), or

- You are physically present in India for a period of 60 days or more during the relevant tax year and 365 days or more in aggregate in four preceding tax years (60-day rule).

Once you meet this criterion, you are legally required to pay tax in India on income earned anywhere in the world, including US interest, dividends, and capital gains.

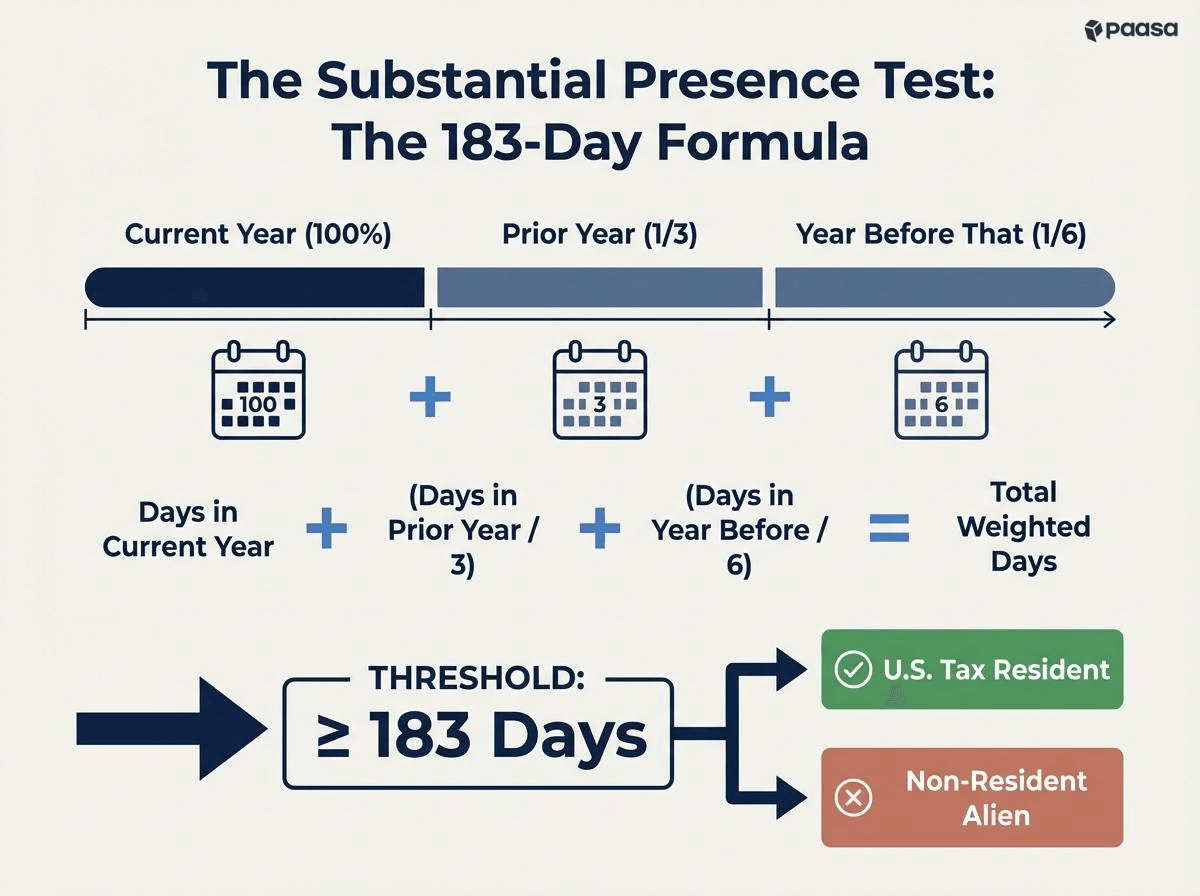

Note: Depending on your travel history, you might land in a situation where you are considered a tax resident of both the US and India.

This happens because the US has a substantial presence rule where you are considered a tax resident if you were physically present in the U.S. on at least:

- 31 days during the current year, and

- 183 days during the 3-year period that includes the current year and the 2 years immediately before that, counting:

- All the days you were present in the current year, and

- 1/3 of the days you were present in the first year before the current year, and

- 1/6 of the days you were present in the second year before the current year.

To learn how you can avoid double taxation and determine your residency in such situations. read our detailed guide on India’s Double Taxation Avoidance Agreements.

What is RNOR status and how does it affect me?

RNOR (Resident but Not Ordinarily Resident) is a transitional tax residency status for returning NRIs. It functions as a bridge between being a Non-Resident and becoming a full Ordinary Resident.

You qualify for this status if you meet one of the following criteria:

- You have been an NRI for 9 out of the last 10 financial years.

- You have lived in India for 729 days or less in the preceding 7 financial years.

- If you are an Indian Citizen or Person of Indian Origin (PIO) with Indian income exceeding ₹15 Lakhs, you become an RNOR if you stay in India for 120 to 181 days (instead of the usual 182).

- If you are an Indian Citizen with Indian income exceeding ₹15 Lakhs and you are not liable to tax in any other country, you are automatically treated as a "Deemed Resident" in India. Deemed Residents are always classified as RNORs.

This status grants you a 1 to 3-year window where your global income is treated differently from that of a standard Indian resident.

What benefits can I get from this status?

As long as you hold RNOR status, your foreign income is NOT taxable in India, provided it is received outside India first. This allows you to manage your US assets without immediate tax liability in India.

- Global Stocks & ETFs: If you sell them while you are RNOR, the capital gains are tax-free in India. You only pay applicable US taxes as a non-resident (0% on gains for non-residents). You can also sell your stocks and ETFs while you hold the RNOR status to reset your cost basis without paying any taxes.

- US Bank Interest: The interest earned in your US accounts is tax-free in India.

- Dividends: Tax-free in India (US withholds 25% tax since you are an Indian resident, upon filing Form W-8BEN).

- 401(k) Protection: Withdrawals from your retirement accounts are not taxed by India during this period.

To utilize these exemptions, you must receive the funds in your US bank account first. If you wire sale proceeds or dividends directly to an Indian bank account, the income is considered "received in India" and becomes fully taxable.

Common Questions US NRIs Have About Moving Back

Can I send money from India and buy more US or overseas stocks?

Yes. You can remit up to $250,000 per financial year under the Liberalised Remittance Scheme (LRS) to invest in foreign stocks. However, be aware that transfers exceeding ₹10 Lakhs in a year attract a 20% TCS (Tax Collected at Source), which you can claim back as a refund when filing your income tax return.

To learn more about how you can send money abroad while complying to Indian regulations, read our Complete LRS Guide for Indians in 2026.

When do I become subject to FEMA upon moving back?

You become a resident under FEMA immediately upon landing in India if your intention is to stay for an uncertain period or for employment/business. Unlike tax residency (which counts days), FEMA residency applies the moment you return to settle.

Can I continue operating my foreign bank account?

Yes. Section 6(4) of FEMA allows you to continue holding and operating foreign bank accounts, stocks, and properties if they were acquired when you were a resident outside India. You are not legally required to close them.

Can I keep my NRO account?

No. Once your status changes to Resident, you are legally required to inform your bank and convert your NRO account to a standard Resident Savings Account. Continuing to hold an NRO account as a resident is a violation of FEMA regulations.

About Paasa

Paasa is a global investing platform built specifically for Indian residents and returning NRIs. We provide direct access to over 10 global exchanges, including the United States, United Kingdom, Switzerland, Hong Kong, Germany, France, Canada, Netherlands, Japan, and Singapore and support 9 global currencies.

- Seamless "In-Kind" Transfers (ACATS): You can move your entire US stock portfolio (from brokers like Robinhood, Schwab, Fidelity, E*TRADE, and more) directly to Paasa. This allows you to consolidate your assets in one place without triggering a tax event.

- The Compliance Advantage: Paasa provides the exact reports you need for your Indian tax returns and foreign asset disclosures, eliminating the need for manual calculations.

- Estate Tax Protection: Paasa offers access to Ireland-domiciled (UCITS) ETFs, allowing you to legally shield your long-term investments from the 40% US Estate Tax that applies to non-residents.

Disclaimer

This article is intended solely for information and does not constitute investment, tax, or legal advice. Global investments carry risks, including currency risk, political risk, and market volatility. Please seek advice from qualified financial, tax, and legal professionals before acting.